Investment Weekly: EM still winning in 2026

11 May 2026

Key takeaways

-

Amid ongoing concerns over the inflationary impact of oil price strength, markets are still expecting a run of rate hikes from Europe’s major central banks in 2026.

-

Asia’s USD-denominated credit markets have held up well amid the global headwinds of policy uncertainty, tariffs and the recent oil spike. While tight spreads could see returns moderate in line with global credit markets this year, there are still good reasons why Asian credit can play a part in portfolios.

-

Japanese policymakers recently stepped into FX markets to help prop up the sagging yen. The question now is whether the latest currency boost will be short-lived, or the start of a durable recovery driven by the Bank of Japan’s policy and improving fiscal confidence.

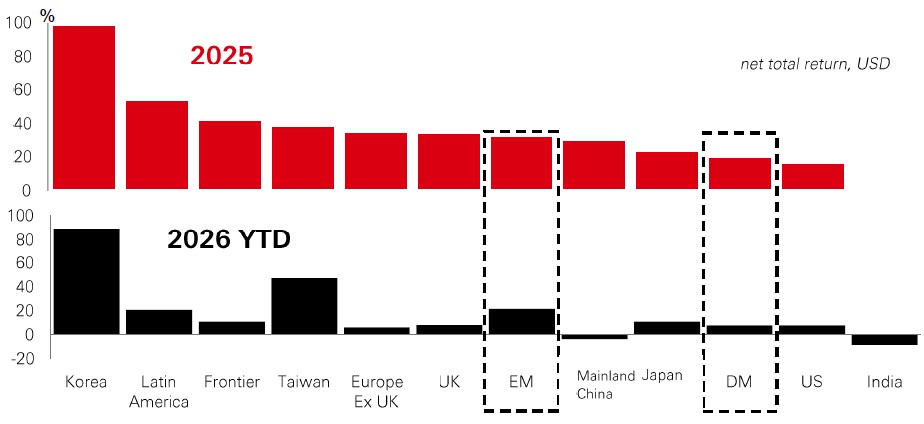

Chart of the week – EM still winning in 2026

A broadening out of market returns was a key development in 2025, driven by a weaker dollar, global central bank policy easing, steady GDP growth, and stronger profits outside of US mega-cap tech. However, the Hormuz crisis is a challenge to this theme in 2026. While US energy independence and the AI boom help insulate the US economy, other regions may face more significant GDP and profits downgrades. Recent US tech earnings have been very solid. And amid a resurgence of inflation, the bar to further central bank rate cuts looks high.

Nevertheless, there are plenty of factors that can keep the broadening out trade alive in 2026. Central banks outside of the US may end up being more hawkish, keeping the dollar-down trend intact. Europe is rearming, which provides fiscal multiplier effects and a new source of earnings growth. Emerging markets (EM) also remain a well-recognised play on the tech and AI theme – given their heavy exposure to South Korea and Taiwan – which is reflected in their year-to-date performance. Simultaneously, the diversification appeal of EM is sustained by valuation discounts, global portfolio under-allocation, and the potential for a multi-year decline in the dollar.

Meanwhile, this year’s surge in commodity prices is not entirely bad news. Markets in Latin America and Frontiers stand to benefit, alongside developed market energy and materials names. And even as the AI boom continues to boost mega-cap tech, the broader infrastructure build-out is lifting industrials, utilities, and materials, while the wider AI adoption and productivity story is positive for sectors far beyond core tech. In short, the AI tide is still rising, but it’s lifting a much wider fleet of boats in 2026.

Market Spotlight

Shock-proofing portfolios

Not all spells of market volatility are equal – and the hedges that can protect portfolios against them don’t always work the same way. Take the V-shaped rebound since markets sold off in March. It has been so quick that diversifiers like hedge funds haven’t needed to do much to protect portfolios. But it’s not always like this…

In 2022, the Russia-Ukraine conflict prompted a huge energy shock and major rate hikes. Volatility surged, and the correlation in performance between stocks and bonds turned positive. On that occasion, commodities and energy stocks offered some protection – but it was also an ideal environment for hedge funds. Strategies like “managed futures” (which trade in futures contracts for commodities, FX, stocks, and bonds) performed especially well.

Looking further back, to a non-energy crisis – the 2008 recession – commodities and energy stocks offered little defence for portfolios. But once again, hedge fund strategies like managed futures delivered strong returns.

It’s a reminder that what works well in portfolio hedges depends on the nature, length, and severity of the shock. Without knowing in advance, allocating to a diversified mix of alternatives and hedge funds makes sense.

The value of investments and any income from them can go down as well as up and investors may not get back the amount originally invested. Past performance does not predict future returns. The level of yield is not guaranteed and may rise or fall in the future. Past performance does not predict future returns. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector, or security. Diversification does not ensure a profit or protect against loss. Any views expressed were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. You cannot invest directly in an index. Source: HSBC Asset Management, Factset, Bloomberg, Macrobond. Data as at 7.30am UK time 08 May 2026.

Lens on…

Curve appeal

Although the ECB and Bank of England may opt for limited tightening to bolster their inflation-fighting credibility, we doubt they can match market pricing. We also see the Fed as more likely to cut than hike, making current government bond yields look increasingly attractive at both the short and long end of the curve.

Technical support

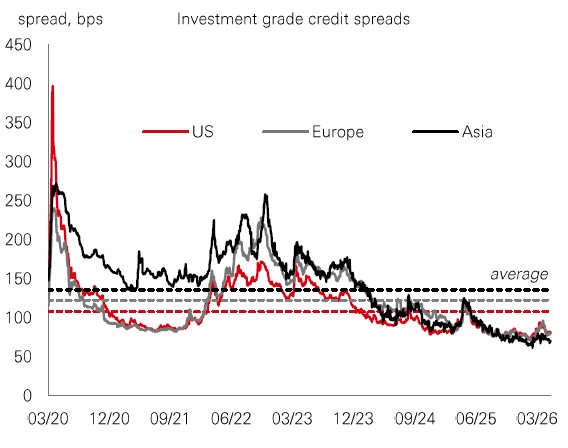

Asia’s USD-denominated credit markets have held up well amid the global headwinds of policy uncertainty, tariffs and the recent oil spike. While tight spreads could see returns moderate in line with global credit markets this year, there are still good reasons why Asian credit can play a part in portfolios. For a start, Asian credit quality is in good shape. Among investment grade issuers, debt levels are stable, balance sheets are solid, and default rates are falling. In high yield, areas of stress are increasingly contained – mainly to Chinese property names – and credit conditions are improving. Second, Asian credit is increasingly diversified across geographies and sectors. High yield has seen a shift away from Chinese property, and some Asian credit experts see encouraging themes in AI and technology, financials, selective renewables and industrials. Thirdly, credit supply in Asia is set to rise this year. While the region isn’t immune to the crowding seen in credit markets elsewhere, rising supply is expected to be met by strong demand. That will give the market added technical support. |

While persistently higher oil prices, tariffs and sticky US rates remain potential risks, Asian credit still offers an eye-catching risk-return profile, supported by improving diversification.

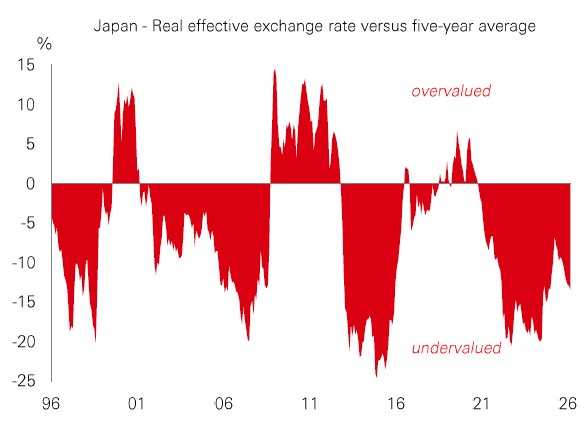

Yen-tervention

Japanese policymakers recently stepped into FX markets to help prop up the sagging yen. The question now is whether the latest currency boost will be short-lived, or the start of a durable recovery driven by the Bank of Japan’s policy and improving fiscal confidence. There are three factors to watch: First, Bank of Japan policy is the main swing factor. April’s hold came with three dissenters favouring a hike. If June passes without action, markets may conclude the BoJ is still behind the curve. Next, global yields matter. Without steady BoJ tightening, sustained yen strength will likely require lower international yields. Progress on reopening Hormuz and/or a major deterioration in global growth could drive this. Finally, fiscal headlines could reintroduce downward yen pressure. June’s cross-party fiscal recommendations may include targeted tax relief, which could revive debt-sustainability concerns. However, recent JGB curve flattening suggests that fiscal worries have eased. |

While the currency looks more stable for now, hurdles remain for a sustained upward trend.

Past performance does not predict future returns. The level of yield is not guaranteed and may rise or fall in the future. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector, or security. Diversification does not ensure a profit or protect against loss. Any views expressed were held at the time of preparation and are subject to change without notice. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. You cannot invest directly in an index. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. Costs may vary with fluctuations in the exchange rate. Source: HSBC Asset Management. Macrobond, Bloomberg, Refinitiv, Factset. Data as at 7.30am UK time 08 May 2026.

Key Events and Data Releases

Last week

This week

For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. Any views expressed were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. You cannot invest directly in an index. Source: HSBC Asset Management. Data as at 7.30am UK time 08 May 2026.

Market review

Global equities saw broad-based gains on signs of easing geopolitical tensions, as oil prices retreated over the week. In the US, momentum in AI stocks and continued strong Q1-26 earnings propelled major indices, including the S&P 500, the Nasdaq and the “Magnificent Seven”, to record highs, with the Philly semiconductor index outperforming. While the Euro Stoxx 50 index rebounded after recent weakness, Nikkei 225 reached an all-time high after the Golden Week holiday. In other Asian markets, the semiconductor-heavy Kospi index surged, alongside decent gains in the Hang Seng, Shanghai Composite, and Sensex. In sovereign bonds, US Treasury yields edged higher, whereas European yields traded modestly lower. In FX markets, major currencies were mixed against the US dollar, while Asian currencies broadly strengthened. In commodities, gold prices rose.

Share

Explore ways to invest

Related Insights

Disclaimer

We’re not trying to sell you any products or services, we’re just sharing information. This information isn’t tailored for you. It’s important you consider a range of factors when making investment decisions, and if you need help, speak to a financial adviser.

As with all investments, historical data shouldn’t be taken as an indication of future performance. We can’t be held responsible for any financial decisions you make because of this information. Investing comes with risks, and there’s a chance you might not get back as much as you put in.

This document provides you with information about markets or economic events. We use publicly available information, which we believe is reliable but we haven’t verified the information so we can’t guarantee its accuracy.

This document belongs to HSBC. You shouldn’t copy, store or share any information in it unless you have written permission from us.

We’ll never share this document in a country where it’s illegal.

This document is prepared by, or on behalf of, HSBC UK Bank Plc, which is owned by HSBC Holdings plc. HSBC’s corporate address is 1 Centenary Square, Birmingham BI IHQ United Kingdom. HSBC UK is governed by the laws of England and Wales. We’re authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the PRA. Our firm reference number is 765112 and our company registration number is 9928412.